Mutual Fund investing is fast catching up in India. Asset Under Management has risen from 1.5 trillion INR in 2005 to 6 trillion INR in 2010 and to 28 trillion INR in 2020 and increasing. Retail participation followed suit and increasingly mutual funds are becoming an integral part of our portfolio.

Investors hunting for the best and most suitable schemes are bombarded with suggestions and recommendations on “Best Schemes”, Top Three Schemes”, Ratings of mutual funds etc. As the recommendations & ratings become dynamic, the “Best Schemes” remain elusive to most investors. To identify the scheme which would offer the best returns among the entire gamut of schemes or even intra-category might seem preposterous to the experienced investor. Instead, retail investors would be better served knowing different types of mutual funds and their suitability to their portfolio.

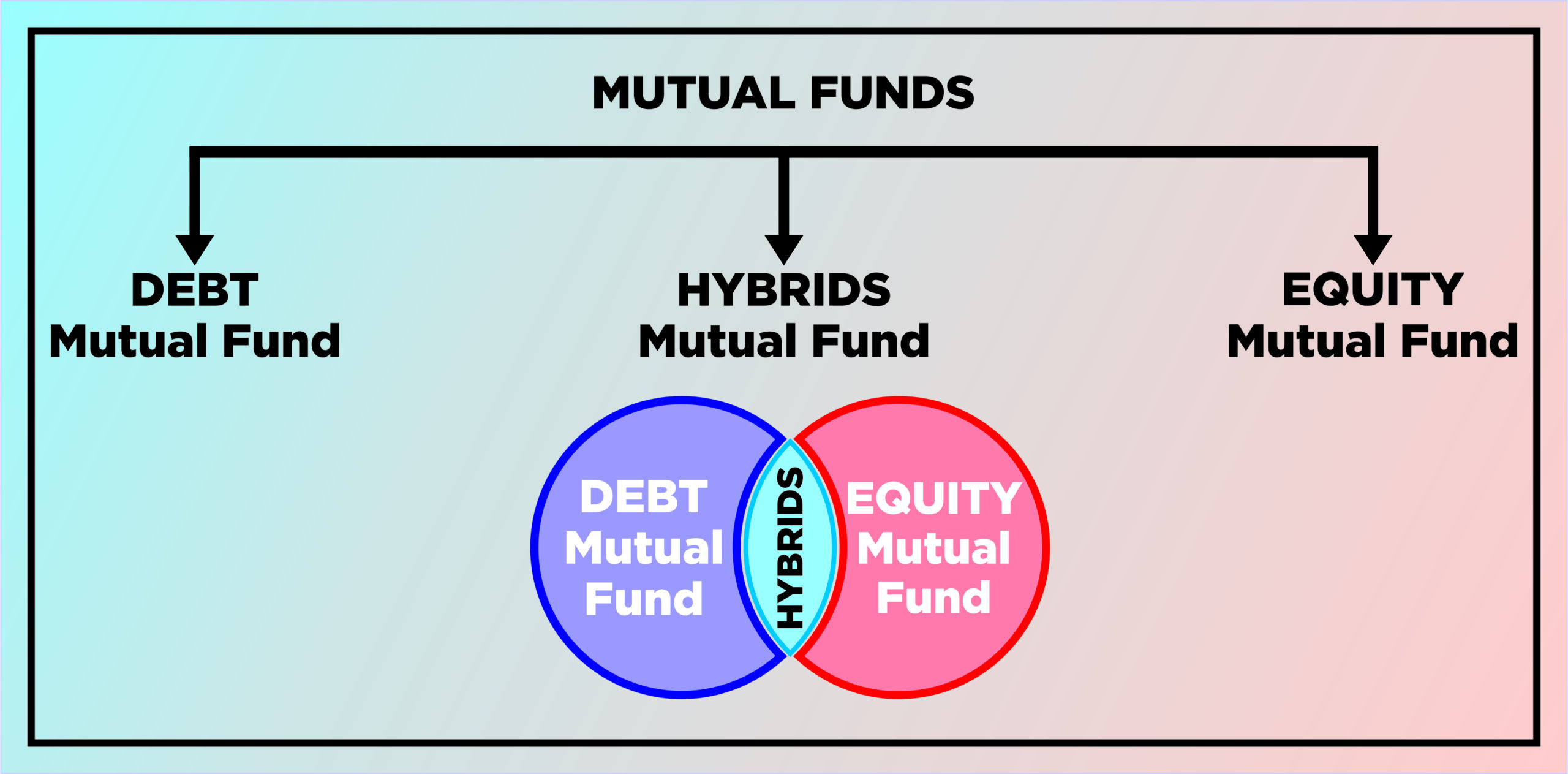

Mutual Fund schemes can be broadly categorised in two categories…Debt Mutual Funds & Equity Mutual Fund. A third category is Hybrids, which is a mix of Equity & Debt.

- What are Debt Mutual Funds

Debt Mutual Funds are a category of mutual funds which invests in debt instruments.

- What are Debt Instruments

Debt instruments are essentially fixed income instruments which are freely tradable. Like fixed deposits they have a fixed tenure, and like fixed deposits they have a fixed interest (coupon) too. However, while a fixed deposit can only be pre-encashed at a reduced rate with the issuer, a debt instrument can be sold in the secondary market at prevailing NAV. Each debt instrument is issued at a Face Value and traded till maturity at NAV.

Debt instruments too are of various types. Instruments of tenures ranging from one day to one year are categorised as Money Market instruments.

Certain debt funds invest in specific debt instruments like Gilt Funds or Corporate Bond funds but most other funds invest in multiple instruments.

- What are the returns from Debt Funds

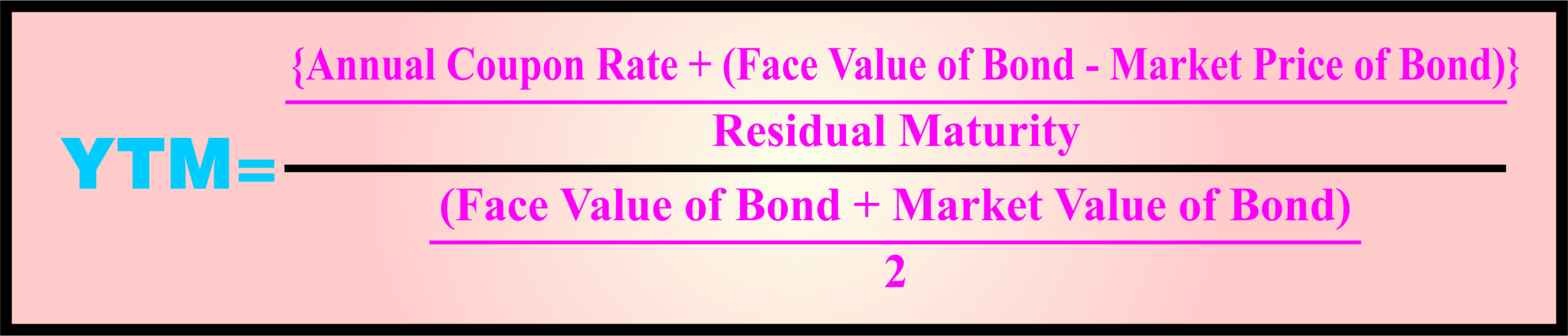

Debt funds returns are market linked and not guaranteed. However, we can ascertain fund returns from the fund’s Yield to Maturity (YTM). If we remain invested till the Average Maturity of the fund, then expected returns from that fund is the (YTM – Expenses).

Actual returns of a Debt fund may vary if redeemed before average maturity or in rare case of default of any instrument.

- Are Debt Funds Risky

If an inherent debt instrument defaults it can affect the fund returns. It is a good idea to check the portfolio of the debt fund and also check the individual instrument ratings before investing. This reduces Default Risk significantly. SOV & AAA for debt instruments and A1 for money market instruments are considered the best ratings.

Bond prices are inversely proportional to interest rate movements. When interest rates fall, it leads to higher bond prices, offering higher notional returns to existing investors but the converse is also true. Hence aligning the fund’s Average Maturity with one’s investment horizon is key and will largely insulate the investor from Interest Rate risk.

The generally accepted notion is higher credit rating offers greater safety of capital but lower YTM.

- Taxation of Debt Mutual Funds

Unlike fixed deposits, in debt funds realised gains are taxed under Capital gains. Hence, you do not incur taxes unless you redeem your fund.

If you redeem your funds in less than three-year period, the realised gains are taxed under short term capital gains, where your gains are clubbed with your income. If however your realised gains are after three years the long-term capital gains consider indexation benefits and your capital gains tax is much lower than income tax payable in case of fixed deposits.

Capital Gains tax computation does not consider your marginal rate of tax as in case of income tax, thereby you pay the same tax irrespective of your tax slab.

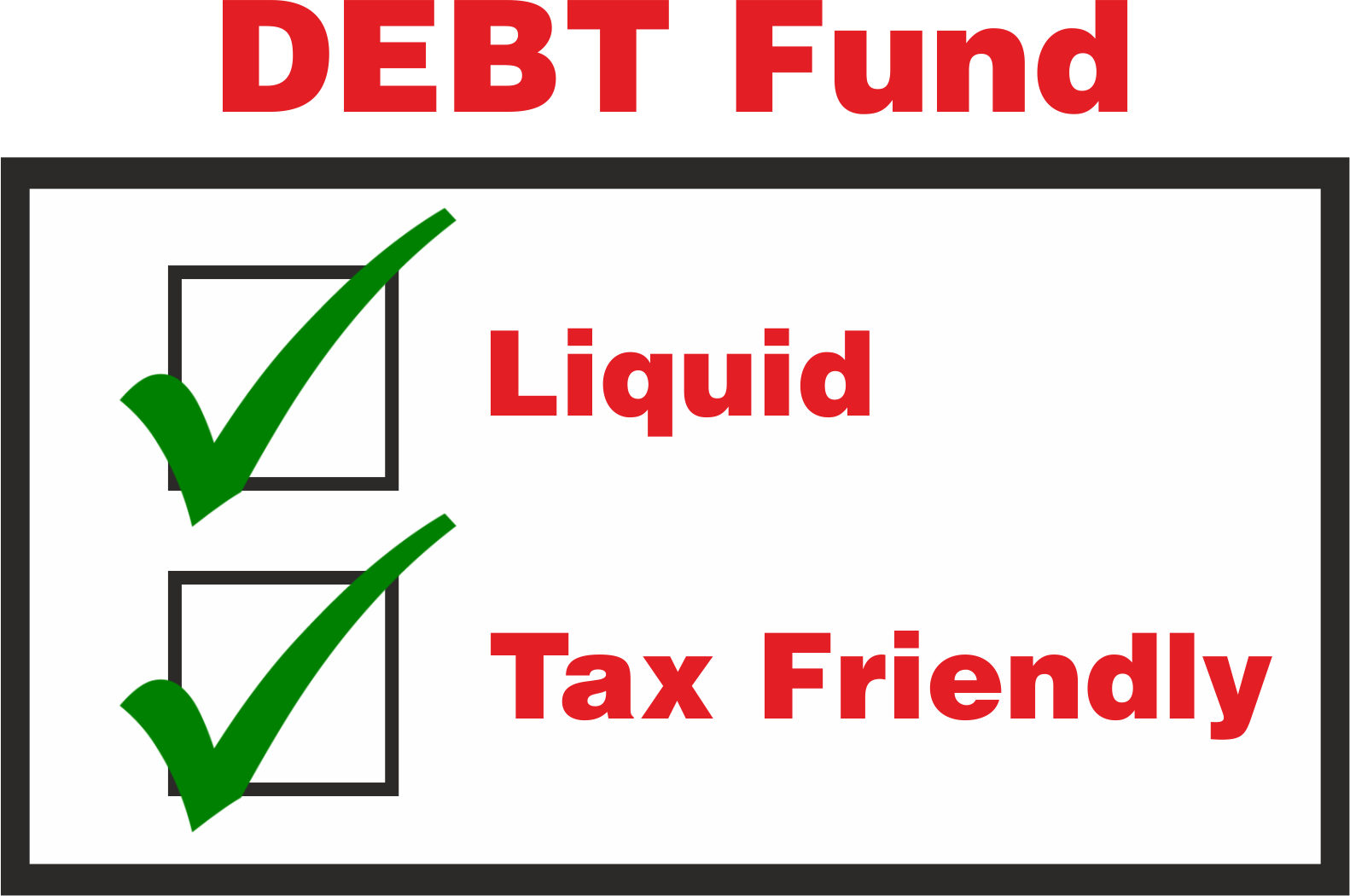

- Are Debt Funds Liquid

Absolutely. You can encash your debt fund at prevailing NAV whenever you wish.

- Should you be investing in debt funds

Debt funds are liquid and tax friendly and therefore offer higher Real Return. If you wish to avoid volatility of equity funds and wish to invest in fixed deposit equivalent, debt funds are an attractive destination. Consider your investment horizon and fund portfolio while selecting your preferred funds. Note past returns do not matter in debt funds.